Market Report 29.05.2026

Osterhorn, Friday, 29.05.2026

The US $ in EURO: 1,1640

What happened this week

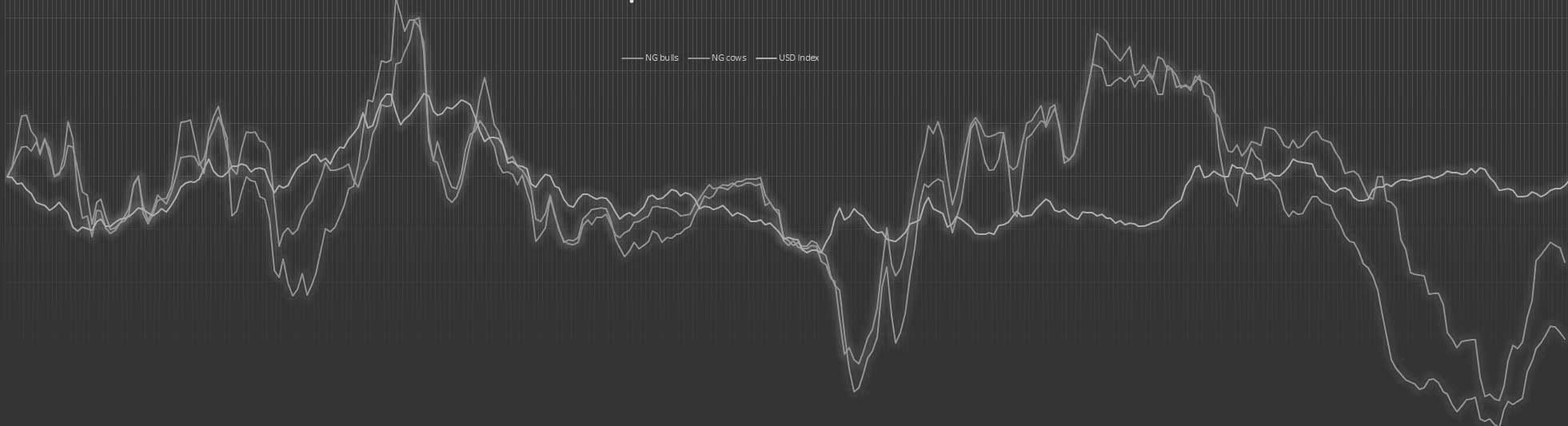

There was once again very little genuinely new to report from the market this week. Overall, the leather industry’s interest in raw material remains unchanged and continues to move at the low level we have been observing for several months now. Demand in Europe appears stable, but stable does not necessarily mean strong. Capacity utilisation in many tanneries is probably around 70%, and in some cases possibly even below that level. Outside of certain niches, the picture in large-scale production remains relatively clear. The market is looking for material that is large and/or thick and good. This is the window that currently describes European leather demand fairly well. However, it also means that only around 50% to 70% of available raw material can be placed into genuinely suitable demand channels. The remaining part of semi-processed material and finished leather is still desperately looking for a market and sales, and in many cases this is only possible at very low prices, or often not possible at all. Inventories of these types still rise. Suppliers of semi-finished selection are trying to counter this situation with better market knowledge, broader sales efforts and more intensive customer work. In some cases, this may help to achieve better results. However, the remaining stocks still available in Europe suggest that this does not work successfully across the board. In Asia, and particularly in China, business remains highly price-driven. Here too, however, the focus is increasingly shifting towards value-adding articles. Demand is concentrating more and more on very specific hide types. This creates a somewhat paradoxical situation. In many regions, the kill is declining, especially in areas where higher-quality raw material is produced. On the one hand, this reduces availability and strengthens the position of suppliers. On the other hand, it does not solve the broader structural issue of insufficient leather demand across all articles. As a result, pressure remains on finished leather prices, while costs continue to rise. At the same time, suppliers are becoming more aggressive in their pricing for those products where the shift in the supply-demand balance is clearly being felt. Without a broader recovery in leather demand, this could point towards a difficult constellation during the summer. In Europe at least, there is currently little to suggest that the kill will increase meaningfully before autumn. This may tighten the situation further ahead of the holiday period, without changing the underlying problems and hurdles of the overall market. From a business perspective, the week was therefore more or less a continuation of what we have already seen. Heavy male material is reasonably well covered by regular customer demand. For lighter and female material, the price competition with Asia continues in unchanged form. With currency and transport costs showing hardly any movement, it remains extremely difficult to bring buyers’ price ideas and the necessary revenue levels of suppliers into alignment. In terms of volume, the week was rather average. Asia was underrepresented in total sales, mainly because the price bids received were not sufficient.

The kill

The kill remains at a low level. This is neither particularly unusual for May, nor surprising in view of the many public holidays. Live cattle prices, especially for male animals, continue to fall sharply. The question now is how far this trend can still go. Overall, prices have now fallen by about 20% from the peak seen in the first quarter. Farmers will increasingly have to consider how to handle this situation over the coming months. For feedlot cattle that are ready for slaughter, there are relatively few alternatives. For grazing cattle, the situation may look somewhat better under normal weather conditions.

What do we expect

Next week will again be interrupted by a public holiday on Thursday in Catholic regions. Many companies are likely to use this as an opportunity to take a bridge day on Friday as well, especially as there is no real need for production. The lower kill continues to support the supply side in certain segments, especially where higher-quality raw material is concerned. However, this support remains highly selective. It does not remove the broader problem that large parts of the selection still lack sufficient demand from the leather industry.As a result, we do not expect any meaningful increase in activity or market movement in Europe. The hope remains that the military confrontation around the Persian Gulf may move towards a pause or an end, which could provide some positive stimulus. However, if market cycles develop in a similar way to previous years, then Asia is also unlikely to show much stronger activity before the end of June. Temperatures are rising, the market is between seasons, and buyers are still waiting for more clarity on consumption and economic stability in the second half of the year before making stronger commitments for raw material and leather products. We therefore do not expect significant price changes next week. Some suppliers may feel that they are regaining a little more leverage in price negotiations, especially where availability is tightening. However, without a broader improvement in leather demand, this leverage is likely to remain limited to selected articles rather nor than becoming a general market movement.

Price Table

| Type | Weight range | Avg. green weight | Salted weight | Avg. weight salted | Price per kg | Trend |

|---|---|---|---|---|---|---|

| Ox | Heifers | 15/24,5 kg | 22,0/23,5 kg | 13/22 kg | 20/21 kg | € 0,80 | stable |

| 25/29,5 kg | 27,5/28,5 kg | 22/27 kg | 25/26 kg | € 0,60 | Stable | |

| Dairy cows | 15/24,5 kg | 22,5/23,5 kg | 13/22 kg | 20/21 kg | € 0,50 | Weakish |

| 25/29,5 kg | 27,5/28,5 kg | 22/27 kg | 25/26 kg | € 0,50 | Weakish | |

| 30/+ kg | 33,5/35,5 kg | 27/+ kg | 29/31 kg | € 0,50 | Weakish | |

| Bulls | 25/29,5 kg | 27,5/28,5 kg | 22/27 kg | 25/26 kg | € 0,80 | Stable |

| 30/39,5 kg | 36,0/37,0 kg | 24/34 kg | 31/33 kg | € 0,80 | Stable | |

| 40/+ kg | 45,0/48,0 kg | 34/+ kg | 38/40 kg | € 0,85 | Stable | |

| Thirds | 15/+ kg | 25,0/27,5 kg | 13/+ kg | 24/26 kg | € 0,35 | Stable |

| Thirds bulls | 30/+ kg | 38,0/40,0 kg | 24/+ kg | 33/36 kg | € 0,40 | Stable |