Market Report 15.05.2026

Osterhorn, Friday, 15.05.2026

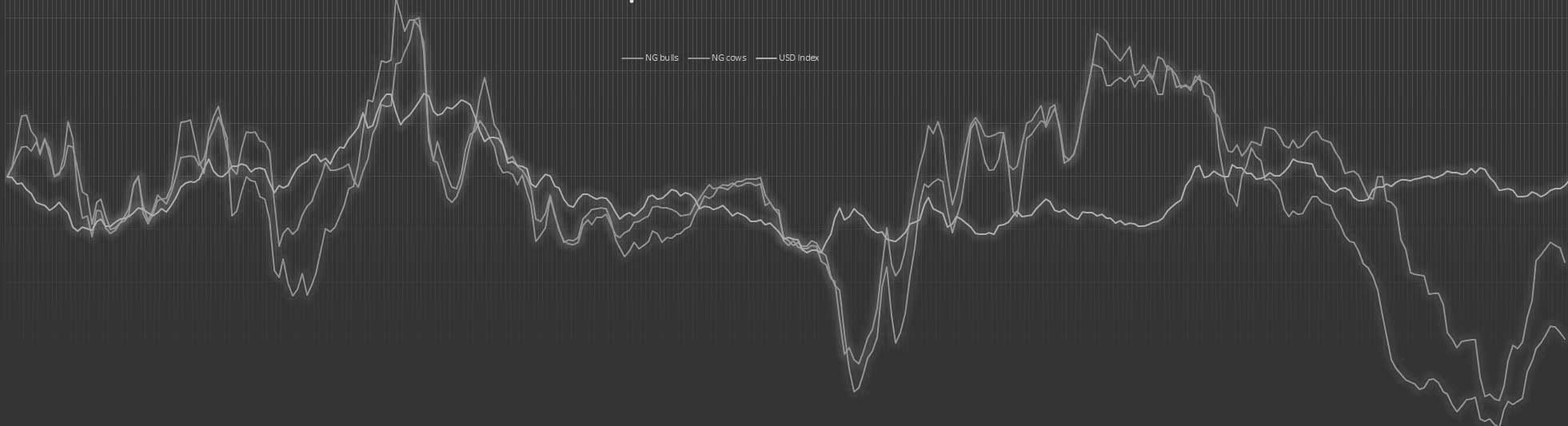

The US $ in EURO: 1,1640

What happened this week

It was another week with a public holiday, this time on Thursday, which effectively shortened the local working week to little more than three days. Internationally, however, most business continued as usual, meaning that the long weekend could not really be used as a proper break. In our small world of hides, skins and leather, business activity remains subdued. At the same time, it is almost weekly possible to observe that structural changes are still taking place. Tanneries are closing, furniture companies are doing the same, and anyone looking for another sign of the ongoing transformation of the market could find it in a further investment by a large Chinese group in the European raw material market, this time in France. Some may still remember what the same investors did in England a few years ago, and long before that with several leather producers in Europe. When capital, strategic interests and political backing come together, it does not necessarily mean that everything will be successful. But such a development is difficult to counter, and it is very likely that this will not be the end of the process. Apart from that, the focus remained on the major political events that everyone can follow directly in the media. As of this afternoon, it is still unclear what decisions and consequences the meeting between two potentates will have for the world economy and, in particular, for the situation in the Gulf. One thing, however, can already be said with some certainty: if the forecasts prove correct that oil prices will remain high and energy supply will stay tight, leather may regain a different kind of relevance. High utility value, durability and longevity could once again carry more weight in an environment of higher energy and material costs. Provided that tanneries are able to produce, leather may also become more competitive again from a pricing perspective. So far, however, hardly anyone seems to have seriously engaged with this angle. The discussions around leather in recent years have been driven by completely different issues, while the questions of product life, durability and relative value have barely been part of the debate. Sales in Europe this week were almost non-existent. From China, the usual tests came again to see what kind of price concessions sellers might be willing to accept. As usual, bids for cow hides were around USD 2.00 to 3.00 below offering prices. It then takes several days before any acceptable package can be put together at all. In most cases, this ends on our side with a reduced quantity in order to limit the “pain” somewhat. A similar pattern applies to the Indian subcontinent and to raw material more suited to the shoe sector. The firmer US dollar towards the end of the week helped a little in individual decisions. The situation is certainly not good, but at least in this way one remains somewhat involved in the market and does not have the feeling of having missed something completely.

The kill

Public holidays, weather, sentiment and prices: at the moment, nothing seems capable of stimulating the kill in any meaningful way. Live cattle prices continue to fall, and the question increasingly becomes what could stop this decline, and when. The new livestock census data will soon become available. This may allow some of the questions that have arisen in recent months regarding the kill to be answered, or at least discussed on a more informed basis. For some time now, cattle numbers, slaughter volumes and the beef business have not really fitted together. In the short term, however, we do not expect any strong recovery. Only if farmers become more nervous and live cattle prices fall even further might there be a willingness to slaughter more “for stock” and consciously take on the corresponding market risk.

What do we expect

At this point in the year, it is difficult to imagine what could stimulate demand in Europe in the short term. In China and Asia, much will depend on how the meeting between Xi and Trump is ultimately interpreted and what impact this will have on trade relations and on the American consumer. The industry there has to take positions and, based on experience, is usually prepared to do so. Nevertheless, it currently does not feel as if much can be expected. China will probably continue to “fish” in the market without creating any major impulses. For the coming week, therefore, the most likely scenario is a continuation of what we have already seen over the past weeks and months: limited activity, difficult negotiations, selective transactions and, overall, a market that continues to search for direction

Price Table

| Type | Weight range | Avg. green weight | Salted weight | Avg. weight salted | Price per kg | Trend |

|---|---|---|---|---|---|---|

| Ox | Heifers | 15/24,5 kg | 22,0/23,5 kg | 13/22 kg | 20/21 kg | € 0,80 | stable |

| 25/29,5 kg | 27,5/28,5 kg | 22/27 kg | 25/26 kg | € 0,60 | Stable | |

| Dairy cows | 15/24,5 kg | 22,5/23,5 kg | 13/22 kg | 20/21 kg | € 0,50 | Weakish |

| 25/29,5 kg | 27,5/28,5 kg | 22/27 kg | 25/26 kg | € 0,50 | Weakish | |

| 30/+ kg | 33,5/35,5 kg | 27/+ kg | 29/31 kg | € 0,50 | Weakish | |

| Bulls | 25/29,5 kg | 27,5/28,5 kg | 22/27 kg | 25/26 kg | € 0,80 | Stable |

| 30/39,5 kg | 36,0/37,0 kg | 24/34 kg | 31/33 kg | € 0,80 | Stable | |

| 40/+ kg | 45,0/48,0 kg | 34/+ kg | 38/40 kg | € 0,85 | Stable | |

| Thirds | 15/+ kg | 25,0/27,5 kg | 13/+ kg | 24/26 kg | € 0,35 | Stable |

| Thirds bulls | 30/+ kg | 38,0/40,0 kg | 24/+ kg | 33/36 kg | € 0,40 | Stable |